NVIDIA enters the one computing market it never owned

NVI DI A is, today, close to a single-product company: the chips it sells to data centres for artificial intelli-gence were about $193.7 billion of its $215.9 billion FY2026 revenue, close to 90% of the business, while everything it sells for personal computers was only about $15 billion. On 31 May 2026, at a major technolo-gy show in Taipei, it moved on the last big computing market it did not already own. NVIDIA unveiled RTX Spark, its first chip built to power personal computers: a single, unusually powerful chip that puts a fast processor and NVIDIA’s world-leading graphics-and-AI engine into one package, going inside premium Windows laptops that ship in the autumn of 2026. Microsoft launched it alongside, with its Surface Laptop Ultra as the flagship machine. I nvestors read it as the start of a new chapter. NVIDIA and Arm, the firm whose chip design it builds on, together added roughly $360 billion of market value in the two trading days around the announcement, with NVIDIA up about 5% on the day. The investment question is not whether the chip is good. I t is whether NVI DI A’s move into the personal computer is a new growth engine worth $360

billion, or a strategically important rounding error. This note argues it is the latter on the numbers and the for-mer on the moat, and that the cleaner trades sit next door, at Apple, Microsoft and Qualcomm.

| $5.4TN VI DI A M ARKET CAPWorld’s most valuable company, 2 Jun 2026 | ~90%DATA CEN TERShare of NVIDIA FY2026 revenue | ~7%GAM I N G & CLI EN TWhere RTX Spark sits in the mix | +$360BADDED ON LAU N CHCombined NVDA + Arm cap, two sessions |

The core insight. The personal computer is the last big computing market NVI DI A did not control. I t already powers the data centres behind AI and the graphics inside gaming machines; RTX Spark completes the set, putting everything NVIDIA makes, the processor, the graphics-and-AI engine and its software, inside a thin laptop. That matters for the long-term position. But NVI DI A sells a chip, not a finished computer. Even a runaway success in laptops is a tiny slice next to $193.7 billion of data-centre sales, and each customer who switches is worth far more to the company they leave than to NVIDIA. The share-price jump has run ahead of the arithmetic. The rest of this note sizes the gap.

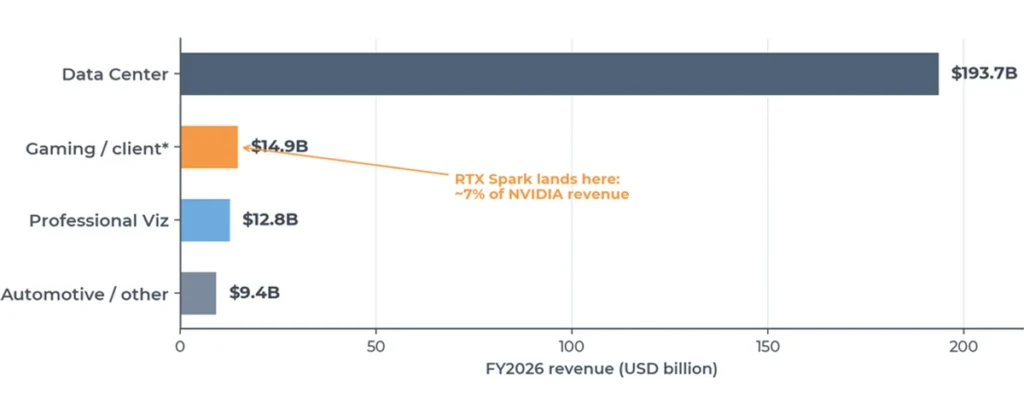

Chart 1: NVIDIA is a data-centre company. RTX Spark plugs into the small client line. FY2026 revenue by segment (USD bn)

Source: NVIDIA Q4 FY2026 results (fiscal year ended late January 2026), Data Center ~$193.7bn of $215.9bn total. *Gaming/client shown as the Q4 FY2026 Gaming run-rate ($3.727bn) annualised to ~$14.9bn; RTX Spark client systems would sit inside this line. Professional Visualization and Automotive/other annualised from Q4 segment prints.

Why the MacBook moat is, for the first time, contestable

For a decade the high-end laptop has been Apple’s by default. Apple’s own in-house chips gave its MacBooks fast performance in a thin, silent, long-battery-life machine, its software kept customers from leaving, and it was the whole package, not any single part, that made it hard to beat. MacBooks are more than half of US premium ($1,000-plus) laptop purchases, and the Mac brought in $33.7 billion of revenue in FY2025. RTX Spark is the first serious answer. I ts decisive advantage is that it runs NVI DI A’s software, the toolkit on which al-most all of the world’s AI is built, which Apple’s machines have never been able to use. For anyone who wants to build or run AI on their own laptop rather than over the internet, that is a real reason to switch, and it aims at exactly the high-end customer Apple has spent years cultivating. Microsoft supplies the other half: a version of Windows rebuilt around AI assistants that can carry out tasks for you, with the Surface Laptop Ultra as the showcase machine.

The advantage is dented, not decisive. Early speed tests put NVIDIA’s new chip roughly level with an Apple chip from two years ago, Apple’s top chip still moves data about twice as fast, and the laptops run a new-er style of Windows on which many existing programs need adapting before they run smoothly. The price does not help: the high-end models are expected to start above $2,899 and cheaper ones near $1,799,

right in MacBook Pro territory rather than undercutting it. The fair near-term verdict is the one industry ana-lyst Ming-Chi Kuo offered: a solid alternative to the Mac for running AI on your own machine, but a niche product.

The bull case is the size of the prize, out to 2030

What the $360 billion jump is really paying for is a foothold in a market NVI DI A has never sold into. The per-sonal-computer market is roughly 270 million machines and $274 billion a year; computers able to run AI on their own cross about 55% of shipments in 2026, around 143 million machines; and the retirement of Windows 10 in October 2025 is pushing a multi-year wave of upgrades. The firm behind this new style of chip aims to take more than half of the Windows market by 2029. I f NVI DI A wins the premium, AI -heavy top

end of that market at a high price per chip, it is a new multi-billion-dollar business sitting on top of the data-centre engine, and it has already promised a faster new generation roughly every year out to 2029. That future possibility, not this year’s sales, is the optimistic case. The cautious case is that the same arithmetic that

makes the data-centre business extraordinary makes the computer business too small to matter.

“The PC is being reinvented. RTX Spark brings everything NVIDIA has built, CUDA, RTX, our AI platform, into a single superchip. With RTX Spark and Microsoft Windows, you ask, and the PC does the work.”

JENSEN HUANG · NVI DI A, COMPUTEX TAI PEI · 31 MAY 2026

Read the partnership carefully. The product needs both names. NVI DI A brings the chip and its software; Microsoft brings Windows, the relationships with every laptop maker, and the AI-assistant features that give people a reason to upgrade. For NVI DI A this is one more product line. For Microsoft it is the first MacBook-class flagship Windows has had in years, and the centrepiece of its plan to put an AI assistant at the heart of Windows. The two companies are not equally affected by whether RTX Spark sells, which is the thread we pull in Section 6.

The P&L reality check: a chip, not a computer

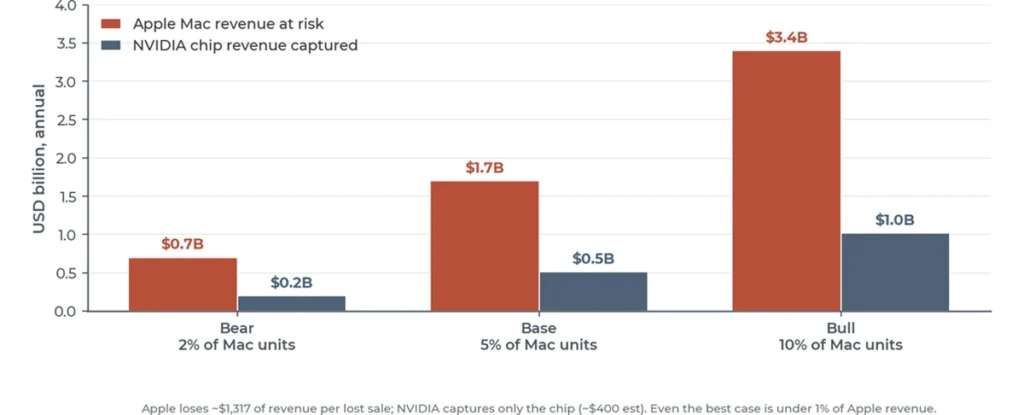

Here the numbers cool the story. NVIDIA does not sell the laptop; it sells the chip to laptop makers like Dell, HP, Lenovo, ASUS and Microsoft, and keeps only the profit on that chip while the laptop maker keeps the profit on the whole machine. Apple is the opposite: it builds the entire machine itself and keeps all the profit, an estimated $1,317 of revenue for every Mac sold. So a high-end buyer who switches from a MacBook to an RTX Spark laptop costs Apple about $1,317 of revenue but hands NVIDIA only an estimat-ed $400 chip. The lost sale is real, but value disappears across the pair: the money that leaves Apple does not

turn up at NVI DI A in anything like the same size. Wolfe Research put the share-price jump in perspective bluntly, and tellingly, the only brokers who raised their price targets after the launch did so for Arm, which earns a small fee on every chip, not for NVIDIA itself.

Chart 2: The mismatch. Apple loses far more per lost sale than NVIDIA gains. Annual $bn at risk vs captured, by scenario

Sowilo estimates. Base: Mac 25.6m units and $33.71bn revenue (FY2025), implied ASP ~$1,317 (Apple discloses neither units nor ASP; IDC units, calen-dar 2025). NVIDIA captured chip ASP assumed ~$400 (no public BOM; well above the ~$50-100 of a Snapdragon part given the large Blackwell GPU). Scenarios = share of would-be Mac buyers diverted to RTX Spark Windows laptops over two to three years.

“Around $360 billion of combined market cap for a PC entry priced above $2,500 implies roughly $1.3 billion ofvalue for every PC sold per year. We see a very limited unit opportunity. The launch is unlikely to move NVIDIA shares.”

CHRI S CASO · WOLFE RESEARCH · JUNE 2026

How much can actually be taken from Apple

The fairest way to size this is to look at what happened last time. The previous laptop to use this new style of chip, from Qualcomm, won just 0.8% of all PCs even after a full launch, and passed 10% only among prici-er $800-plus laptops; industry researchers expect this whole new chip category to stay under 13% of the market in 2025, against about 87% still using the traditional design. RTX Spark starts from a stronger posi-tion than Qualcomm did, NVI DI A’s brand and graphics, Qualcomm’s lock on Windows now expired, and far better software for running existing programs, but a higher price. On that track record we sketch three cas-es for the share of Mac sales NVIDIA pulls away over two to three years: a cautious 2%, a middle 5%, and an optimistic 10%. Even the optimistic case is about 2.6 million machines, roughly $3.4 billion, under 1% of Apple’s total revenue, and the Mac is only about 8% of Apple to begin with. The share NVI DI A can take is genuine. The money involved is small on both sides, and smaller for NVI DI A than for Apple.

Chart 3: Ambition versus the track record. Where this new kind of Windows chip sits today against the >50%-by-2029 target

Source: Snapdragon X share Q3 2024 (Counterpoint / industry data via Tom’s Hardware); Arm-on-Windows 2025 ceiling (ABI Research); >50%-by-2029 ambition (Arm CEO Rene Haas, Reuters, 2024). The 50% bar is a stated target, not a forecast or a print.

Sowilo’s read

Three conclusions for how to position around the rise of NVI DI A in computing.

We value NVIDIA for its AI-fuelling chip business. The investment case is still the roughly $194 billion AI business that powers data centres. RTX Spark strengthens NVI DI A’s long-term position, it puts its software in one more place and adds a fourth growth leg with a roadmap out to 2030, but it is not a meaningful profit dri-ver in 2026 or 2027. We believe the market is going through interesting times and has started assigning sub-stantial value to the personal computer too, while we would still prefer to value the franchise for its AI -fuelling chip business. We also believe the whole AI value chain has become very pricey, and it generally does not fit our philosophy of deep value investing.

The threat to Apple is to the story before it is to the profits. The Mac is about 8% of Apple and the realistic loss is under 1% of revenue, so this is not an earnings event. The real exposure is to perception: Apple is widely seen as behind in AI , its long-promised Siri upgrade has slipped into 2026, and RTX Spark lets a Windows lap-top claim the lead in running AI on your own machine. That is a story that can weigh on Apple’s valuation be-fore it ever shows up in the numbers, and it is the thing to watch at Apple’s developer conference.

The clearer opportunities are at the edges. Microsoft is the quiet winner: it finally has a MacBook-class flagship for Windows and a centrepiece for its AI -assistant plans, even though laptops are a small part of a company driven by a roughly $169 billion cloud business. Qualcomm is the loser: the new-style Windows lap-top was meant to be its growth story, and it has just lost its most powerful future rival to NVI DI A, which the market marked on day one by sending Qualcomm’s shares down about 7% while NVI DI A rose. The straight NVI DI A bet here is small. The trades around it, long the winners and wary of the loser, are where the launch actually moves value.

What to watch. How well RTX Spark laptops actually sell, and at what price, this autumn against the

$2,500-plus starting point; whether NVIDIA ever reports its computer-chip sales as a separate line, the sign they are becoming big enough to matter; Apple’s AI response at its developer conference and any answer such as a Mac with more built-in memory; and the reviews of Microsoft’s Surface Laptop Ultra as the test of whether this new kind of Windows laptop has finally produced a genuine MacBook rival, or just another niche.

Regards,

Team Sowilo

Disclaimer: Any information contained in this material represents Sowilo’s views and research analysis and shall not be deemed to constitute advice, an offer to sell or purchase, or an invitation or solicitation to do so, for the securities of any entity. Sowilo Investment Managers LLP and its employees

and directors shall not be liable for any loss, damage or liability whatsoever, direct or indirect, arising from the use of this information. Sowilo Investment Managers LLP, SEBI Registered Portfolio Manager (INPO00008127). www.sowilo.co.in – SEBI Registered PMS Company in India